The saying, “If you love what you do, you will never work a day in your life” holds for those looking to build a stable and fulfilling career.

However, a successful career isn’t just about skill-building and climbing the corporate ladder. Your ability to sustain long-term growth also depends on how well you manage your finances. Poor financial health can lead to stress, limited career choices, and setbacks in professional development.

What can make this 10 times worse is dealing with a financial emergency without any backup or savings to fall back on and a poor credit score.

Although some small debt options like a £500 loan may come to your rescue, it’s not ideal to be dependent on debt to deal with unexpected expenses.

That’s why, in this article, we’ll explore why financial well-being should be an important part of your career plan and how it impacts your professional life.

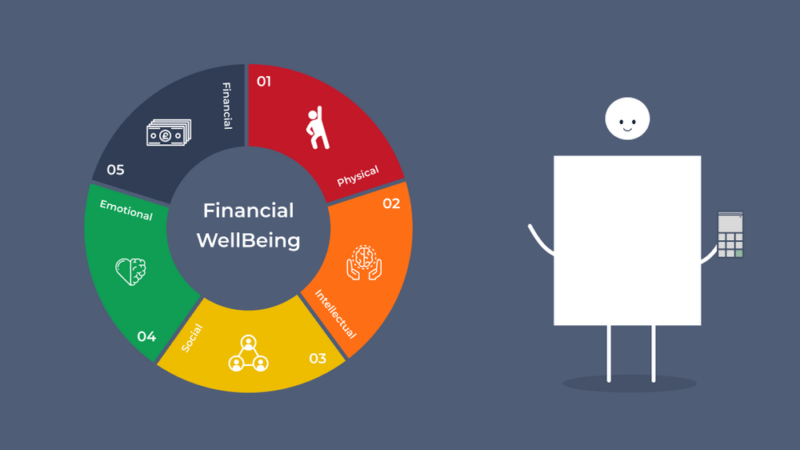

What Is Financial Wellbeing?

Financial wellbeing is the ability to manage day-to-day expenses while maintaining stability for the future. It involves ensuring you can afford necessities such as rent or mortgage payments, household bills, and essential purchases without financial strain.

Beyond covering basic needs, financial wellbeing also includes having an emergency fund, saving for future goals, hobbies, and having the flexibility to enjoy life without guilt.

How Financial Stability Fuels Career Success?

1. Strengthens Your Job Prospects

Being in a solid financial position can make you a stronger job candidate. Many employers include credit checks as part of background screenings, so a poor credit history could potentially raise red flags. Financial security is especially important for roles that involve financial responsibilities or security clearances.

2. Gives You the Freedom to Be Selective

Job hunting can be stressful, especially when financial pressures force you to take the first opportunity that comes your way. With strong personal finances, you gain the freedom to wait for the right role rather than settling for a job out of desperation.

3. Allows You to Leave a Bad Job

When finances are tight, leaving a job that no longer serves you may not feel like an option. On the contrary, financial security gives you the ability to walk away from toxic work environments or unfulfilling positions without immediate consequences.

4. Enhances Your Negotiation Power

When you’re financially stable, you have the confidence to negotiate salaries, raises, and promotions without the fear of rejection. Being financially dependent on a job can make people hesitant to ask for what they truly deserve. But, when your finances are in order, you can advocate for better compensation without worrying about the consequences of a “no.”

5. Enables Professional Development

A stable financial foundation gives you the freedom to invest in personal and professional growth. Whether it’s taking online courses, attending industry conferences, or obtaining additional certifications, financial security allows you to expand your skill set and increase your value in the job market.

6. Helps Maintain Focus and Prevents Burnout

Financial stress can be a major distraction at work, affecting productivity and job performance. Constantly worrying about bills, debt, or unexpected expenses can make it difficult to concentrate and deliver your best at work. When your financial wellbeing is in check, you can fully focus on your job without the worry of affording the necessities.

7. Creates Long-Term Financial Growth

A strong financial foundation sets you up for long-term wealth-building and income diversification. As you progress in your career and earn more, having healthy financial habits allows you to invest, save, and create additional income streams beyond your primary salary.

Job loss, medical emergencies, or unexpected expenses can occur at any time, and when unforeseen circumstances like these arise, they can have a major effect on your finances. In such cases, personal loans can serve as a short-term financial tool to bridge the gap without derailing your career progress. While they should be used responsibly, they can provide essential relief in difficult times, allowing you to stay financially afloat and focus on regaining stability.

Build a Money Cushion Before You Need It

Emergency funds prevent panic. Without one, any setback becomes a crisis. Start by calculating three to six months of essential expenses. That’s your minimum cushion.

Follow these steps to begin:

- Open a separate savings account.

- Automate small weekly transfers.

- Set a short-term target before expanding.

- Pause unnecessary subscriptions or luxuries.

- Use windfalls like tax refunds or bonuses to boost savings.

Once your fund exists, your career decisions won’t be driven by fear. It also reduces dependence on debt-based solutions during hardship.

Set Career Goals Around Financial Milestones

Financial targets create focus. Most people build careers with titles or promotions in mind. Shift the lens. Make money milestones part of your plan.

Track goals such as:

- Clearing all high-interest debt

- Saving a set percent of income

- Investing in a personal development fund

- Building a passive income stream

- Reaching a stable monthly budget with surplus

Each goal connects your finances to your growth path. Align salary discussions, role changes, or learning with these markers. Over time, it reshapes how you define success.

Don’t Let Lifestyle Inflation Kill Progress

More money doesn’t mean more freedom—unless you manage it right. Lifestyle inflation ruins momentum. A raise or a new job often leads to bigger spending. Instead of building wealth, people stay stuck in the same financial stress cycle with just fancier bills.

Lock in your savings before adjusting any expenses and keep your housing and car costs modest. Also, it is better to focus on long-term investments instead of short-term rewards. Always question upgrades—ask yourself if it’s truly a need or just a status symbol. Discipline in these areas strengthens your future choices. You avoid staying in jobs just to fund habits you never needed in the first place.

Use Financial Tools as Leverage, Not Crutches

Loans, credit cards, and advances aren’t evil. But they must serve a purpose. Use short-term tools only to protect long-term plans. For instance, a personal loan can prevent you from pausing education or relocating for a better role.

Key rules:

- Borrow only what you can repay without pressure.

- Always read the interest terms.

- Don’t rely on credit to maintain appearances.

- Pay off debt before taking on new ones.

Financial tools should work for you—not replace proper planning. Used wisely, they can help you stay on track instead of falling behind.

Final Thoughts

Career success isn’t just about skills and experience; it’s also about financial preparedness. By managing money wisely, improving credit health, and planning for future goals, you set yourself up for success in both your professional and personal life. A career plan is not just about making money; it’s about creating a stable and sustainable future that allows you to thrive.